Problem

Customer feedback and servicing data pointed to a consistent theme: borrowers felt our loan product lacked adaptability. This feedback, paired with competitive analysis of fintech leaders offering more personalized repayment experiences, signaled both a user need and a strategic opportunity.

We proposed a design sprint to explore “smart repayment” features, with a hypothesis that personalization could:

- Help differentiate our product in a crowded market

- Improve funnel performance

- Increase customer satisfaction (NPS)

Problem Statement

As a customer paying off a personal loan.

I want to manage my loan repayment in a way that matches my financial circumstances.

But the repayment schedule is rigid and inflexible, with only one static payment plan.

Because life events, income fluctuations, and financial goals vary from person to person.

Which makes me feel stuck, unsupported, and less in control of my financial journey.

Research

We partnered with a third-party research vendor to conduct foundational discovery, including in-depth interviews and behavioral segmentation. Their findings helped surface key opportunities around repayment flexibility and identified two promising concepts for further exploration:

- Decreasing Monthly Payments

- Payment Holiday

Key insights included:

- Users felt disempowered by fixed repayment structures.

- Financial flexibility increased emotional engagement and perceived fairness.

- People preferred options that made progress visible or offered temporary relief during known financial stress points.

I worked closely with the research team to synthesize findings, align them to business goals, and translate them into actionable experience principles:

- Momentum matters: Visualize progress early and often.

- Life happens: Give users tools to adapt when circumstances change.

- Design for autonomy: Offer smart choices with clear guidance.

These insights laid the foundation for our design and testing roadmap.

Design

Design Objective

Create a more flexible, human-centered repayment experience that increases customer confidence, encourages early engagement, and improves funnel conversion—without introducing complexity or regulatory risk.

With the two user-driven repayment options identified, I led the internal design team through concept validation and interaction design.

We explored:

- How each concept would be introduced in the apply funnel

- Decision friction vs. user control

- Compliance and backend constraints

Through internal ideation sessions and lightweight prototyping, we shaped both experiences into scalable, testable components:

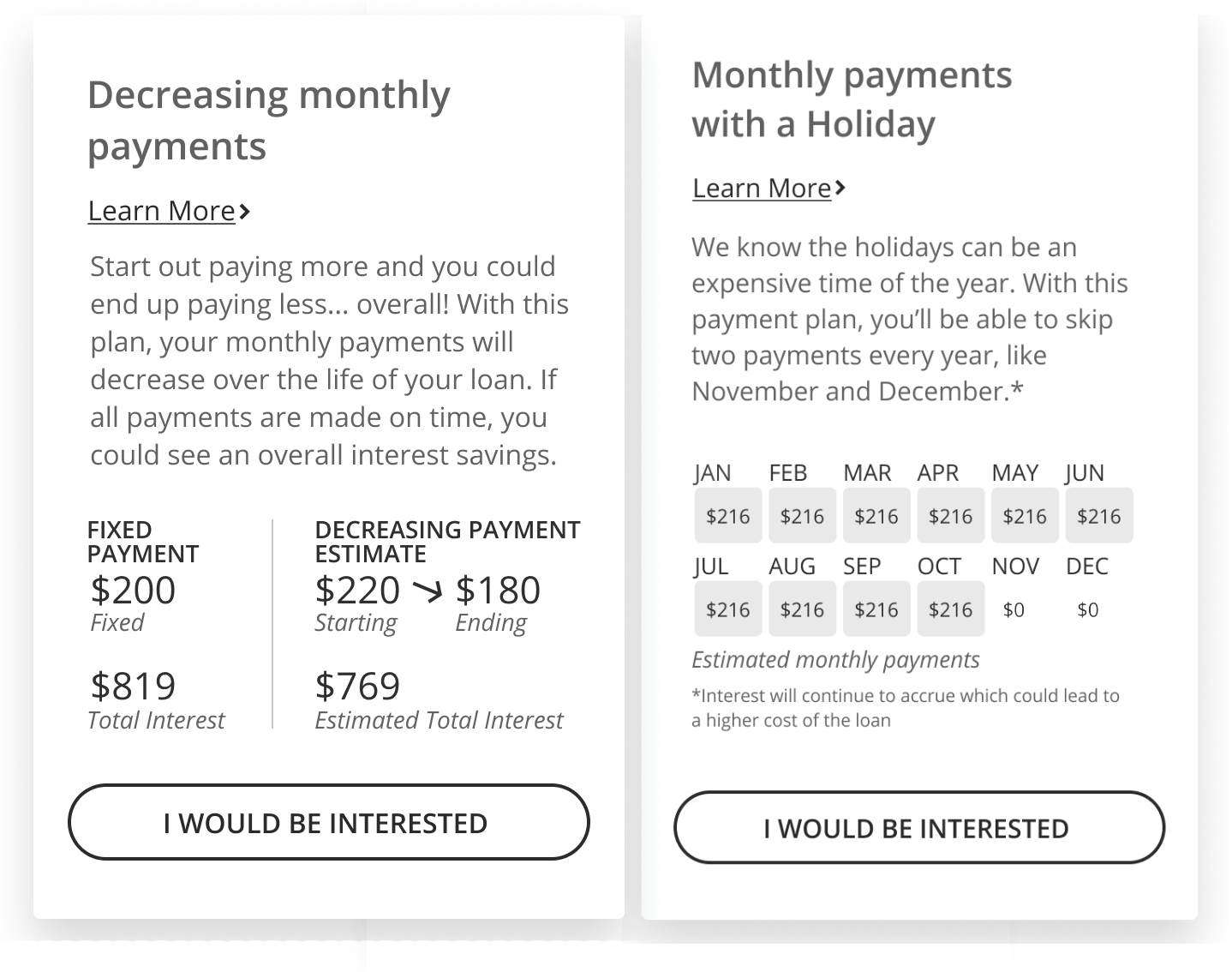

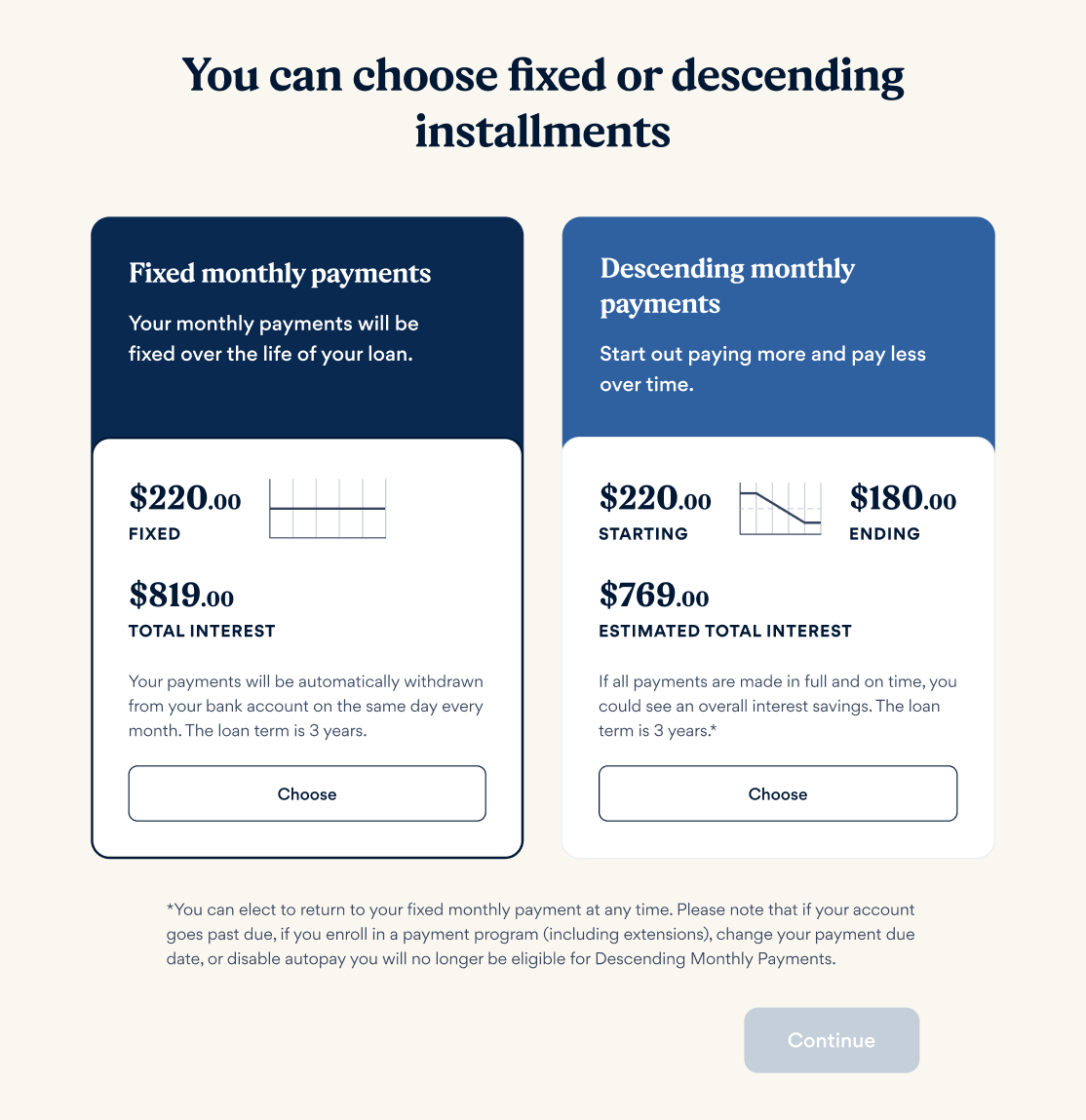

1. Decreasing Monthly Payments

Starts with slightly higher payments that decrease over time—users feel early momentum and long-term relief.

2. Payment Holiday

Allows borrowers to skip one payment per year—offering planned relief without penalty.

I collaborated with product and engineering stakeholders to assess technical feasibility and define MVP criteria for live testing. We prioritized clarity, minimal funnel disruption, and legal alignment in our designs..

Testing

User Survey:

We ran a preference survey alongside:

- 63% of respondents chose one of the smart options over the fixed plan

- Users cited “feeling in control” and “easier to manage” as top reasons

This multi-method approach helped us triangulate desirability, feasibility, and potential impact before investing further.

Painted Door Test:

We introduced a lightweight “choice screen” into the live application funnel to test engagement without backend functionality.

- 53% of engaged users selected Decreasing Monthly Payments

- 23% selected Payment Holiday

- No significant increase in funnel abandonment

Results

We proceeded with an A/B test of Decreasing Monthly Payments, given its stronger signal.

Outcomes:

- Verification rate +1.58%

- Funded/offered rate +1.18%

- NPS +16 points

These were statistically significant improvements in both conversion and customer sentiment.

My Role

- Defined the design strategy and success metrics with product and data leads

- Facilitated co-design and prioritization workshops

- Guided junior designers on prototyping and usability testing

- Presented findings to senior leadership to secure buy-in for continued investment

- Balanced user desirability with compliance constraints and tech feasibility